2025 Mid-Year Venture Insights

Tracking the pulse of VC, M&A, and CVC as 2025 unfolds

The first half of 2025 is now behind us — and in many ways, it has defied the expectations we set just a few months ago. This is part one of my midyear series, where I’ll break down:

✅ Exit activity

✅ Funding trends

✅ CVC (corporate venture capital) participation

Let’s dive in.

Exits

Initial Public Offerings

Key Points

Volume down

Amount raised up, but…

Healthtech, Fintech, and Automation dominated

At the start of 2025, I was convinced we’d see a rush of IPOs as the market unclogged and pent-up private companies seized an open window. That didn’t happen. Exit activity was more muted than expected, leaving a significant backlog of VC-backed firms still on the sidelines.

There were 18 VC-backed IPOs in the U.S. during the first half, raising around $6.4 billion. Nearly a quarter of that value came from just one deal — CoreWeave’s $1.5 billion offering. For context, there were 25 VC-backed IPOs in the same period of 2024, raising about $5.2 billion.

So, while the dollar amount rose year over year, much of that gain was thanks to CoreWeave. Without it, 2025 would have lagged in both total proceeds and deal count.

Key verticals among IPOs? HealthTech and Life Sciences led, showing the resilience of healthcare innovation. FinTech and financial technologies stayed active, with a focus on embedded finance and blockchain solutions. And unsurprisingly, Artificial Intelligence and automation remained hot, transforming everything from enterprise SaaS to supply chains.

M&A

Acquisition activity continues to be the primary path to exit. There were 496 acquisitions of U.S.-based VC-backed companies in the first half. That is a strong showing and reinforces that M&A now accounts for the lion’s share of venture exits, outpacing IPOs and pushing secondaries to third place. (For more on secondaries, see my recent article here).

Of those 496 M&A transactions, 342 targeted AI or SaaS startups — no surprise given current market excitement about automation, infrastructure, and next-gen software.

Funding Activity

Key Trends

Valuation up

Deal volume up

Elevated demand and supply imbalance

Valuations and deal activity both increased. However, one persistent challenge is the demand/supply imbalance for venture capital. According to Pitchbook’s 2025 U.S. Venture Capital Outlook Midyear Update, the ratio of dollars sought by startups to dollars available from VCs is 1.7x, about 31% above the historical average of 1.3x.

In simple terms: for every $1 available from investors, $1.70 of capital is being sought by startups.

I suspect this mismatch is driven by a mix of constrained GP (general partner) budgets (given limited exit opportunities) and the flood of new startups made possible by AI lowering barriers to entry.

For corporate investors, this imbalance could create opportunity. More startups are competing for a relatively fixed pool of funding, potentially giving CVCs more influence and leverage. That said, the capital crunch is not uniform: AI and high-growth technology startups continue to attract premium valuations and find money more easily, while less “hot” sectors may see better pricing and healthier terms for new investors.

Another result of the imbalance? More consolidation. We should expect continued acquisitions, particularly of startups that struggle to gain market traction.

Valuations by stage:

Series A Post-Money: median hit $75M, up from $65M (+15.4%) year over year.

Seed Post-Money: median rose to $26.5M, up from $20M (+32.5%).

Seed New Money: median was $5.7M, up from $4M (+42.5%).

Series A New Money: median edged up to $12.2M from $11M (11%).

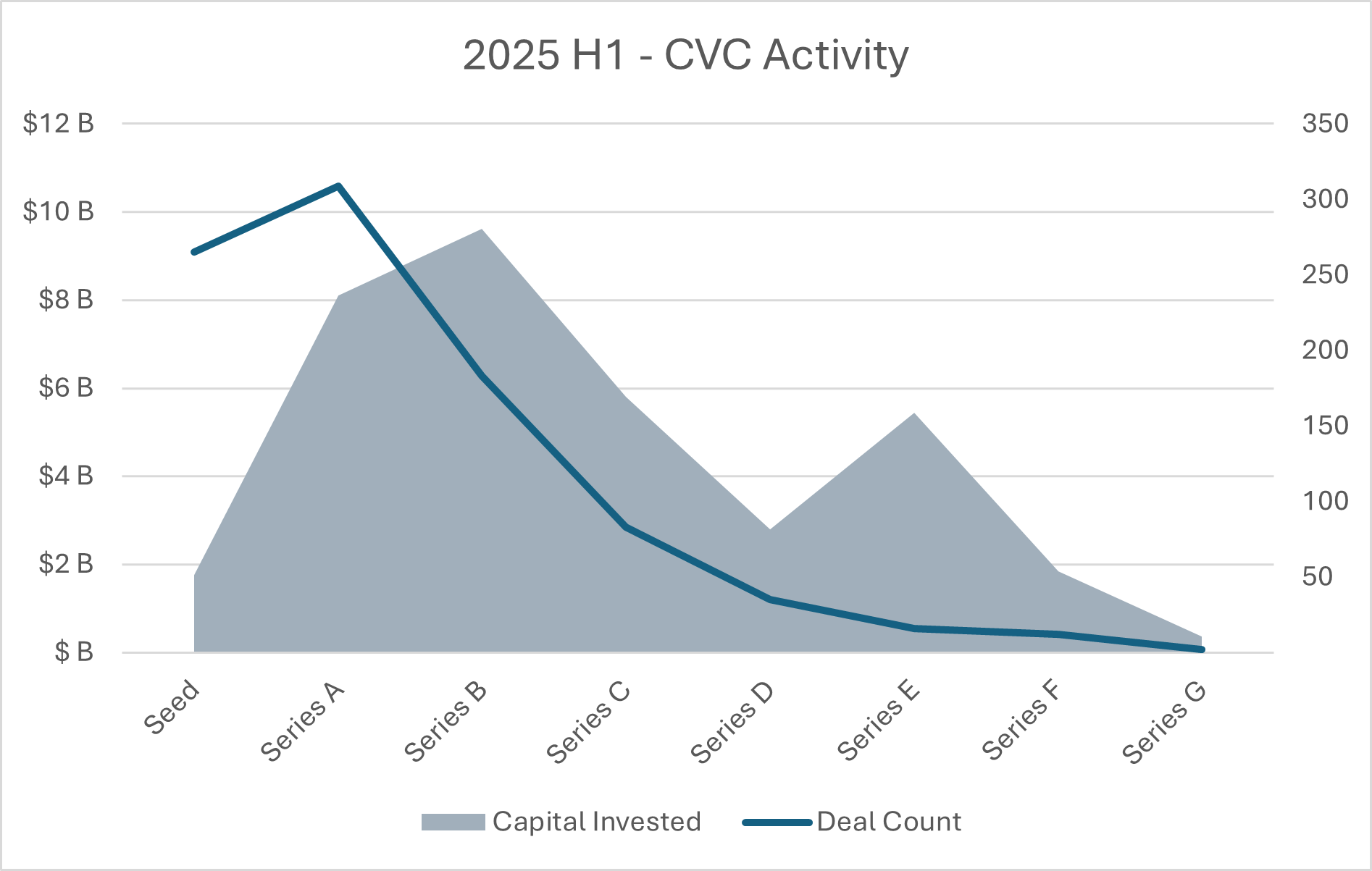

CVC Activity

In the first half of 2025, 905 corporate venture programs made at least one investment, down from 1,053 in the first half of 2024.

These CVCs deployed roughly $35.7 billion in capital. Nearly 63% of deals involved emerging and early-stage startups, but those deals only represented 27% of the total capital deployed. In other words, while most CVC deals are going into earlier-stage opportunities, the bigger checks are still going to more mature companies.

Final Thoughts

The first half of 2025 has been a reminder that especially in venture capital, predictions are hard. While IPO volumes underwhelmed, M&A continues to be the dominant exit path, and secondaries remain an important liquidity tool. Funding continues to flow, albeit with a growing mismatch between supply and demand, and CVCs appear well positioned to benefit.

As we move into the second half of the year, I’ll be watching:

Whether IPO volumes rebound

How much valuations stabilize

Whether the capital demand/supply ratio tightens